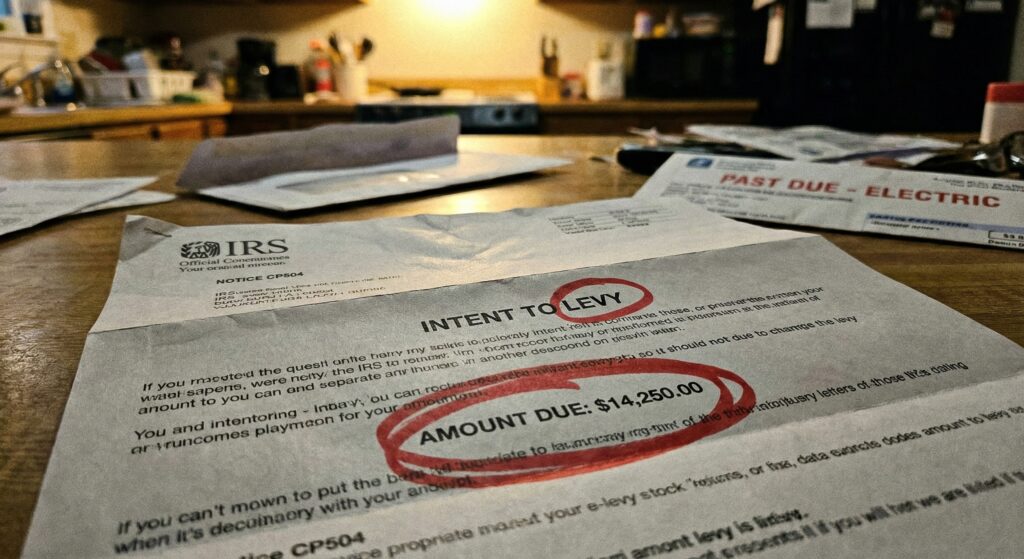

I am not a tax professional. I am someone who opened their mailbox on a Tuesday afternoon in February and found a CP504 Notice the IRS’s formal declaration of intent to levy. Bold text, official seal, the works. AMOUNT DUE: $14,250.00. They were threatening to seize my state refund and garnish my wages.

My first reaction was to Google “tax relief” which was a mistake. Within ten minutes I had three browser tabs open for companies promising to “settle my debt for pennies on the dollar” for an upfront fee of $3,500 to $5,000. I almost called one of them.

I did not. What I found instead was a legitimate, government-run tool that showed me the IRS’s own math and that math said they should accept my $250.

Here is the whole story, with the numbers that are actually correct.

Step One: Use the IRS’s Own Calculator Before You Do Anything Else

The IRS Offer in Compromise (OIC) program allows the agency to legally accept less than the full amount you owe but only if a specific formula says you cannot reasonably pay the balance. Before you hire anyone, before you call anyone, go to the official IRS OIC Pre-Qualifier tool at irs.treasury.gov/oic_pre_qualifier.

This tool uses the same calculation IRS agents use. You input your income, expenses, assets, and liabilities. It outputs whether you likely qualify and what a realistic offer amount looks like.

My inputs:

- Monthly income: $2,100

- Monthly allowable expenses (rent, food, transportation): $1,800

- Monthly disposable income: $300

- Assets: a 2009 car worth roughly $2,000, no home equity, no investments

The tool told me I would likely qualify and suggested a lump-sum offer in the $250–$500 range. I offered $250. After a four-month review, the IRS accepted. The remaining $14,000 was discharged.

The OIC Application: What the Articles Leave Out

The application fee is $205, and it is non-refundable whether the IRS accepts or rejects your offer.

However and this is the part most articles bury in a footnote if you qualify as a low-income taxpayer (at or below 250% of the federal poverty level based on household size), the IRS waives not just the $205 application fee but also the 20% initial payment you are normally required to send with a lump-sum offer.

That means in my case, I submitted the application at zero upfront cost. The $250 was only due after acceptance. Without that waiver, I would have owed $50 (20% of $250) with the application itself which does not sound like much, but it matters when you are broke.

What you submit: Form 656 (the actual offer), Form 433-A (your complete financial disclosure), the application fee or low-income waiver certification, and your initial payment or waiver.

The Backup Plan: Currently Not Collectible Status (Status 53)

If you have equity in a home, a retirement account, or other assets even if you have no monthly cash to spare the IRS may reject your OIC on the grounds that you could liquidate those assets to pay the debt. That is when you look at Currently Not Collectible (CNC) status, also known internally as Status 53.

CNC means the IRS formally acknowledges you cannot pay without suffering genuine financial hardship meaning you could not cover basic living expenses if they collected. Collection activity stops immediately: no garnishments, no levies, no bank seizures.

What you actually need to do to get it:

The article circulating online says “just call the IRS.” That is incomplete. You must also submit Form 433-F a Collection Information Statement which discloses every income source, every asset, every monthly expense. The IRS reviews this to confirm hardship is real, not claimed.

The 10-year rule and its crucial nuance:

The article version of this story says the debt “vanishes after 10 years.” That is broadly true but imprecise in a way that matters. The 10-year Collection Statute Expiration Date (CSED) runs from the date the IRS assessed the tax debt not from when CNC status was granted.

Additionally, certain events pause that 10-year clock: filing for bankruptcy, submitting an OIC application, requesting a Collection Due Process hearing, or living outside the United States for six months or more. If any of those apply to you, your clock may be longer than you think, and this strategy becomes less clean.

One more critical point: CNC does not erase the debt while active. Interest and penalties continue to accrue. If your financial situation improves and the IRS detects it through your annual tax filing, they will remove you from CNC and demand payment.

Which Program Actually Fits Your Situation?

The Warning About “Tax Relief” Companies

The ads that appeared in my search results after I opened that CP504 were not scams in the legal sense. Some of those firms have real enrolled agents who do real work. But the services they charge $3,000 to $5,000 for preparing Form 656, submitting Form 433-A, negotiating an OIC are things you can do yourself for $205 or less using the IRS’s own tools and publicly available instructions.

The only scenario where professional representation clearly earns its fee is when your situation is genuinely complex: a business with multiple tax years, significant assets to negotiate around, a pending audit, or a tax debt that resulted from fraud or a divorce dispute. For a straightforward individual hardship case with W-2 income and no major assets, the Pre-Qualifier tool and the IRS’s own forms are sufficient.

Use the tool first. Then decide if you need help.

This article reflects IRS programs and fee schedules as of the 2026 filing season. Fees and program details are subject to change. Always verify current information at IRS.gov or consult a licensed CPA, enrolled agent, or tax attorney before filing any IRS resolution application.

Evan Cole Editor-in-Chief | Breaking News & Public Policy

“From Washington to Wall Street, and Main Street to Hollywood—Evan Cole connects the dots.”

As the Editor-in-Chief at Newskilo, Evan leads a dynamic team of journalists dedicated to uncovering the truth behind the headlines. With over 15 years in digital media, Evan has a reputation for cutting through the noise.

While he is widely recognized for his deep analysis of U.S. fiscal policy (IRS & Stimulus), Evan’s expertise extends to global current events, corporate accountability, and cultural trends. Whether he is breaking down a complex government bill, exposing a tech giant’s failure, or analyzing the societal impact of a viral celebrity moment, Evan’s goal is simple: To tell the stories that shape our world with clarity, accuracy, and integrity.