The most ambitious component of the “One Big Beautiful Bill Act” is finally going live.

On July 5, 2026, the U.S. Treasury will begin funding “Trump Accounts,” a new tax-advantaged savings vehicle designed to make every American child a shareholder in the national economy. For babies born in 2025 and later, this account comes with a $1,000 government seed deposit.+1

However, unlike the automatic stimulus checks of the pandemic era, this money requires action. You must affirmatively elect to open the account by filing specific IRS paperwork. If you miss this step during the current tax season, your child’s account will start at $0.

The “Seed” Eligibility: Who Gets the $1,000?

Confusion remains high regarding who gets the free government money versus who simply gets an empty investment account. The law draws a hard line based on birth year.

The “Pilot” Group (Gets $1,000)

- Requirement: Born between January 1, 2025, and December 31, 2028.

- Status: Must be a U.S. Citizen with a valid Social Security Number.

- Benefit: The Treasury deposits $1,000 directly into the account on or after July 5, 2026. This money is tax-free and does not count toward your annual contribution limit.

The “General” Group (No $1,000)

- Requirement: Any child born before 2025 who is still under age 18.

- Benefit: You can open a Trump Account to enjoy tax-deferred growth and employer matching, but the account starts with a $0 balance. The government does not seed accounts for older children.

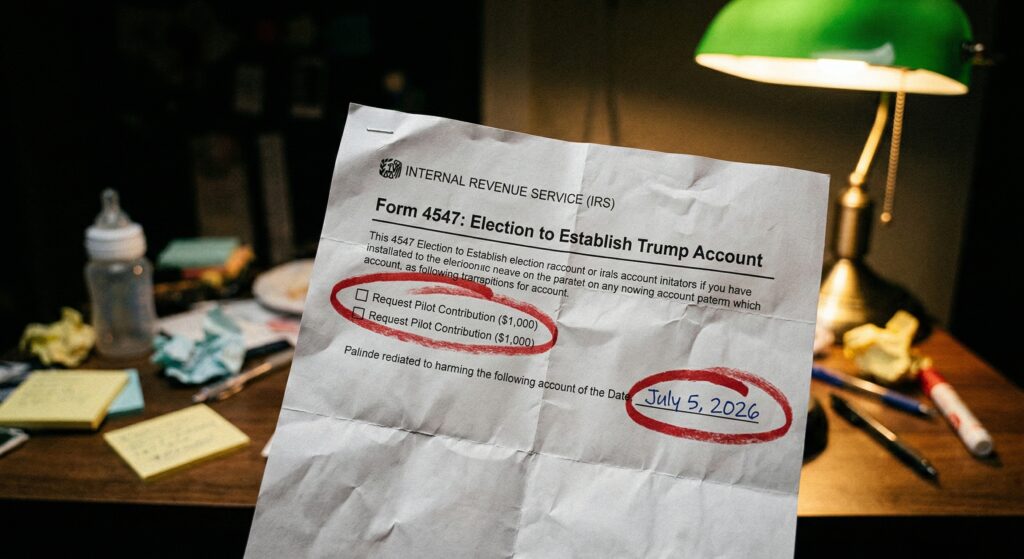

How to Claim It (IRS Form 4547)

For the 2026 tax season (filing 2025 returns), you cannot simply walk into a bank to sign up. You must make an official election with the IRS.

Step 1: File Form 4547

This new form is titled “Election to Establish Trump Account.” You must attach it to your Form 1040 tax return.

- Crucial Section: Look for Part III. You must check the box explicitly requesting the “Pilot Program Contribution” for your eligible child.

Step 2: The July 5 Trigger

The Treasury will not fund any accounts before Independence Day weekend. Deposits begin rolling out on July 5, 2026. If you file Form 4547 now, you are essentially pre-registering to be in the first wave of funding.

Investment Rules: You Cannot Pick Stocks

These accounts are designed for passive, long-term growth. To protect the government’s investment, the OBBBA restricts how the funds are managed until the child turns 18.+1

- Allowed: Low-fee index funds tracking the S&P 500 or total U.S. stock market.

- Banned: Individual stocks (no Tesla, Gamestop, or Apple), crypto, or options trading.

- The Logic: The government wants these funds to track the American economy broadly, not gamble on specific companies.

Trump Accounts vs. 529 Plans

Parents often ask if this replaces a college savings plan. It does not. They serve different purposes.

| Feature | Trump Account (New) | 529 Savings Plan |

| Federal Seed | $1,000 (Newborns only) | $0 |

| Use of Funds | Retirement / General Wealth | Education Only |

| Investment Choice | Index Funds Only | Varies by Plan |

| Tax Treatment | Tax-Deferred (Taxed on withdrawal) | Tax-Free (for Education) |

| Rollover | Becomes IRA at age 18 | Can rollover to Roth IRA (limited) |

Employer Matching: The Hidden Tax Break

The most powerful feature of the Trump Account is not the $1,000 seed. It is the employer match.

- The Rule: Employers can contribute up to $2,500 per year to your child’s account.

- The Benefit: This contribution is tax-free to you. It does not count as taxable income on your W-2, yet it belongs to your child instantly.

- Family Limit: The total combined contribution (parents + employer) cannot exceed $5,000 per year.

State Tax Warning ⚠️

While federal law treats employer contributions as tax-free, state legislatures move slower.

Residents in “non-conforming” states like California, New York, and Minnesota may still owe state income tax on employer contributions made to these accounts. Until local laws are updated, you might have to add that “free” $2,500 back into your state taxable income.

Disclaimer: This article covers OBBB provisions for the 2025 tax year filed in 2026. Always verify details at IRS.gov.

Evan Cole Editor-in-Chief | Breaking News & Public Policy

“From Washington to Wall Street, and Main Street to Hollywood—Evan Cole connects the dots.”

As the Editor-in-Chief at Newskilo, Evan leads a dynamic team of journalists dedicated to uncovering the truth behind the headlines. With over 15 years in digital media, Evan has a reputation for cutting through the noise.

While he is widely recognized for his deep analysis of U.S. fiscal policy (IRS & Stimulus), Evan’s expertise extends to global current events, corporate accountability, and cultural trends. Whether he is breaking down a complex government bill, exposing a tech giant’s failure, or analyzing the societal impact of a viral celebrity moment, Evan’s goal is simple: To tell the stories that shape our world with clarity, accuracy, and integrity.