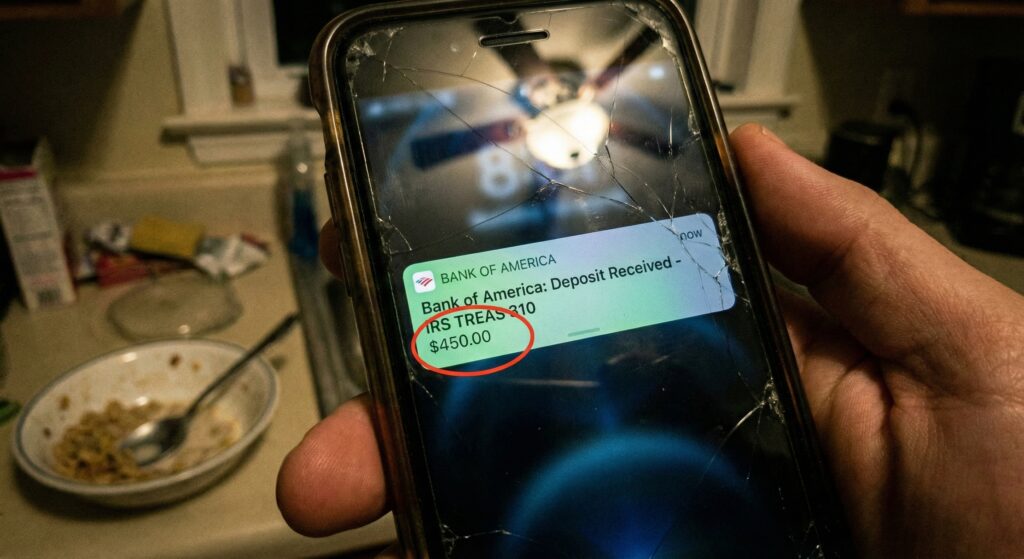

You filed in late January, expecting the “One Big Beautiful Bill” tax cuts to finally put real money in your pocket. Instead, you got a $450 deposit notification. No drama, no error message just a number that does not match what you were planning.

Before you call the IRS or assume your software glitched, understand that there are four specific, fixable reasons this happens. Let me walk through each one honestly.

Reason 1: The IRS Quietly Gave You Your Refund Early

This is the most common cause, and almost nobody talks about it clearly.

When the OBBBA raised the standard deduction in 2025, the IRS updated its withholding tables the formulas your employer uses to calculate how much federal tax to pull from each paycheck. If your employer updated payroll software correctly, your take-home pay was slightly larger every two weeks throughout 2025.

That extra $30 or $40 per paycheck? That was your refund arriving in installments rather than as a lump sum in February. It is mathematically equivalent but it feels like you got less because there is no exciting deposit notification in January.

What to do: If you strongly prefer a lump-sum refund over fatter paychecks, you have to manually override the system. Log into your employee payroll portal, open your 2026 Form W-4, and use Step 4(b) the Deductions Worksheet to enter your expected OBBBA deductions (tips, overtime, auto loan interest). This tells your employer to withhold as if you have fewer deductions during the year, creating a larger refund at filing time.

Reason 2: The Overtime Deduction and Your W-2 (This Is Where Most Articles Get It Wrong)

If you claimed the new qualified overtime deduction and your refund looks light, your first instinct might be to blame your W-2. Some articles are telling readers to demand a corrected W-2 (Form W-2c) if Box 14 is empty. That advice is wrong.

Here is what the IRS actually said in Notice 2025-62 and Notice 2025-69: for Tax Year 2025 only, employers were not required to separately report qualified overtime on Box 14 of your W-2. Some employers did it voluntarily; many did not. Both approaches are legal and correct.

If your Box 14 is blank, you do not need a W-2c. You can and should calculate your qualified overtime compensation using:

- Your final 2025 pay stubs showing overtime amounts

- Your employer’s payroll portal showing a breakdown of regular vs. overtime hours

- Any written statement your employer provided separately

Enter that amount on Schedule 1, Line 18 of your Form 1040, following the IRS Notice 2025-69 methodology. If you already filed without claiming this deduction because you thought the blank Box 14 disqualified you, then you file a Form 1040-X to amend and reclaim what you missed.

Reason 3: The Treasury Offset Program Took Your Money

This one hits without warning. Since May 2025, the Bureau of the Fiscal Service has fully resumed intercepting tax refunds to cover defaulted federal debts a pandemic-era pause that is definitively over.

If your refund was intercepted, the most common causes are:

- Defaulted federal student loans (private loans cannot do this only federal)

- Unpaid child support certified by a state agency

- Past-due state income taxes

- Overpaid federal benefits (Social Security, unemployment)

You should receive a mailed Notice of Intent to Offset at least 60 days before the seizure, but those notices sometimes get lost or go to old addresses.

What to do: Call the Bureau of the Fiscal Service’s Treasury Offset Program hotline at 800-304-3107 to confirm what debt was collected and by which agency. If the offset was applied in error for example, against a loan you already consolidated or rehabilitated you can dispute it directly with the debt-holding agency, which has authority to reverse the offset.

Reason 4: Gig Income Without Quarterly Payments

If you earned more than $20,000 selling on eBay, Etsy, or Poshmark, or drove for Uber, DoorDash, or similar platforms, and you did not pay quarterly estimated taxes throughout 2025, the IRS applied your entire annual tax bill against your refund at once plus a potential underpayment penalty on top of it.

Your refund is not just smaller; it may have flipped negative. Self-employment tax (15.3% on net earnings) plus your marginal income tax rate can consume nearly a third of gig income before the QBI deduction. If this surprised you this year, the solution for 2026 is four quarterly payments in April, June, September, and January using Form 1040-ES.

How to Engineer a Larger Refund in 2027

If you want a guaranteed lump-sum refund and you are a W-2 employee, the most reliable method is controlled over-withholding via your W-4.

- Log into your payroll portal and open your 2026 Form W-4

- Go to Step 4(c) Extra Withholding

- Enter an additional flat dollar amount per pay period

| Extra Per Paycheck | Pay Frequency | Extra Withheld Per Year |

|---|---|---|

| $25 | Bi-weekly (26×) | $650 |

| $50 | Bi-weekly (26×) | $1,300 |

| $100 | Bi-weekly (26×) | $2,600 |

The IRS returns this as a refund with no conditions. It is not a loan it is your own money coming back to you in one check. The tradeoff is that you are giving the government an interest-free loan throughout the year. Whether that is worth it depends entirely on your financial discipline and whether a forced savings mechanism actually helps you.

One Final Check Before You Conclude Your Return Is Wrong

A smaller-than-expected refund is not automatically an error. The IRS does not owe you a specific amount it owes you the difference between what you paid and what you owed. If that gap closed because you got more money in each paycheck, you are not worse off. You are actually holding more of your own money at zero interest instead of lending it to the federal government.

But if you suspect a missed deduction for overtime, tips, or the auto loan interest credit, do not file an amended return impulsively. Check your return line by line first. In many cases, a tax professional can identify the gap in under 20 minutes far cheaper than the anxiety of waiting on a 1040-X.

This article covers the 2025 tax year filed in early 2026. Tax rules and IRS guidance may change. Always verify details at IRS.gov or consult a licensed CPA before making filing decisions.

Evan Cole Editor-in-Chief | Breaking News & Public Policy

“From Washington to Wall Street, and Main Street to Hollywood—Evan Cole connects the dots.”

As the Editor-in-Chief at Newskilo, Evan leads a dynamic team of journalists dedicated to uncovering the truth behind the headlines. With over 15 years in digital media, Evan has a reputation for cutting through the noise.

While he is widely recognized for his deep analysis of U.S. fiscal policy (IRS & Stimulus), Evan’s expertise extends to global current events, corporate accountability, and cultural trends. Whether he is breaking down a complex government bill, exposing a tech giant’s failure, or analyzing the societal impact of a viral celebrity moment, Evan’s goal is simple: To tell the stories that shape our world with clarity, accuracy, and integrity.