The email arrived on a Tuesday. “Your Form 1099-DA is ready.”

What followed wasn’t a tax bill. It was a number that didn’t reflect reality.

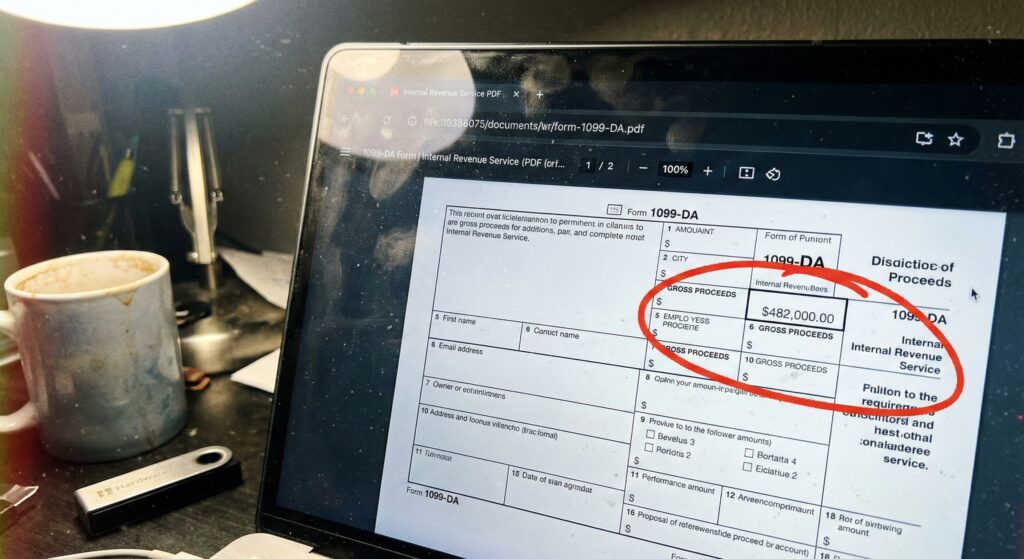

Gross proceeds: $482,000.

For a trader who’d actually lost roughly $5,000 over the year chasing meme coins, panic-selling Ethereum, riding the volatility down that figure looked like a system error. It wasn’t. It was the IRS’s new digital asset reporting infrastructure working exactly as designed.

The Gap Hidden in the New Form

Form 1099-DA, officially titled Digital Asset Proceeds From Broker Transactions, debuted for the 2025 tax year. Under final regulations issued by the Treasury in 2024, U.S.-based custodial brokers including major cryptocurrency exchanges are required for the first time to report each customer’s gross proceeds directly to the IRS.

What they are not required to report, for this first filing cycle, is your cost basis.

The gap between those two numbers is everything. Under Treasury Decision 9992 and the phased implementation of §6045, basis reporting is not required for any digital asset sold in calendar year 2025 meaning every 1099-DA issued for 2025 transactions will show proceeds without a corresponding purchase price. Mandatory basis reporting only kicks in starting with 2026 transactions, and even then only for “covered securities” digital assets acquired on or after January 1, 2026, and held continuously within the same broker account.

Anything bought before that date, or ever transferred off-platform, is a noncovered security, for which brokers are not required to report basis.

The practical consequence: a taxpayer who bought Bitcoin at $95,000 and sold it at $96,000 made $1,000. Their 1099-DA shows $96,000. If the broker didn’t or couldn’t voluntarily report the $95,000 basis, that full $96,000 lands in IRS data systems without any context.

What the Mismatch Triggers

The IRS doesn’t manually review every return. It runs automated matching programs the Automated Underreporter (AUR) system being the primary tool that cross-reference broker-reported data against what taxpayers actually file. A 1099-DA showing $96,000 in proceeds against a return reflecting a modest gain, or none at all, registers as a discrepancy.

That discrepancy doesn’t automatically mean an audit. It typically generates a CP2000 notice a formal IRS letter asking the taxpayer to explain the difference. Ignoring it, however, or filing as if the 1099-DA never existed, is a different matter entirely.

The Question at the Top of Your Return

Form 1040 has included a digital asset disclosure question since the 2019 tax year. For the 2025 return, it reads: “At any time during 2025, did you receive, sell, exchange, or otherwise dispose of any digital asset?”

If a broker has already submitted a 1099-DA with your name and Social Security number, checking “No” creates an immediate, machine-readable contradiction between your return and the agency’s records. Tax attorneys describe this as one of the most straightforward audit triggers currently in the IRS’s arsenal.

2025 Crypto Transactions at a Glance

| Transaction Type | Taxable Event? | How It’s Taxed |

|---|---|---|

| Buying crypto with USD | No | Not taxed until sold |

| Trading BTC for ETH | Yes | Capital gains (sale price minus cost basis) |

| Staking rewards | Yes | Ordinary income, valued at time of receipt |

| Spending crypto on a purchase | Yes | Treated as a sale capital gains apply |

| Wallet-to-wallet transfer | No | Not taxable; transaction fees may be deductible |

How to Fix a Blank Cost Basis

A 1099-DA showing large proceeds and zero basis is not a final verdict it’s an opening position. You can correct it, but you’ll need to do the legwork.

Start by downloading your full transaction history from every exchange you used in 2025. Most platforms offer a CSV export directly from account settings. From there, dedicated crypto tax software Koinly, CoinTracker, TaxBit, and others can reconstruct your actual cost basis by matching purchases to sales across wallets and exchanges.

The correction is documented on Form 8949, where you list the gross proceeds (matching the 1099-DA exactly) alongside your calculated cost basis, yielding the accurate gain or loss figure. That Form 8949 flows into Schedule D of your 1040. Filing it correctly, with supporting transaction records, is what converts a scary-looking notice into a non-event.

The Real State of IRS Enforcement

Set aside the narrative about an army of crypto-hunting agents. Under DOGE-driven workforce reductions in 2025, the IRS lost approximately 11% of its overall staff and roughly 31% of its revenue agents, the employees who conduct audits through just the first quarter of 2025 alone, per a May 2025 report from the Treasury Inspector General for Tax Administration. By February 2026, the agency’s IT division had shed close to 40% of its technology staff.

That context matters. But it doesn’t mean digital asset enforcement has gone quiet.

The IRS’s Criminal Investigation division runs Operation Hidden Treasure, which uses commercial blockchain analytics firms to trace wallet activity and cross-reference transactions at scale. A closer look at the enforcement picture reveals that data-matching infrastructure not auditor headcount is the primary mechanism for catching 1099-DA mismatches. Automation doesn’t require a full roster.

One more date worth marking: starting with transactions executed in 2026, brokers must report both gross proceeds and cost basis for covered securities. That 2027 filing season will look meaningfully different. For now, the burden of proof rests entirely with the taxpayer and it starts with a spreadsheet.

This article is for informational purposes only and does not constitute financial or legal advice. For authoritative guidance, consult the IRS Digital Assets resource center or a qualified tax professional.

Evan Cole Editor-in-Chief | Breaking News & Public Policy

“From Washington to Wall Street, and Main Street to Hollywood—Evan Cole connects the dots.”

As the Editor-in-Chief at Newskilo, Evan leads a dynamic team of journalists dedicated to uncovering the truth behind the headlines. With over 15 years in digital media, Evan has a reputation for cutting through the noise.

While he is widely recognized for his deep analysis of U.S. fiscal policy (IRS & Stimulus), Evan’s expertise extends to global current events, corporate accountability, and cultural trends. Whether he is breaking down a complex government bill, exposing a tech giant’s failure, or analyzing the societal impact of a viral celebrity moment, Evan’s goal is simple: To tell the stories that shape our world with clarity, accuracy, and integrity.