WASHINGTON —

California business entities and individual employers face a strict July 10, 2026, statutory deadline to recover thousands of dollars in improperly assessed tax penalties. Federal court decisions, intersecting with recent structural changes authorized by the Trump administration’s Treasury Department, have created a narrow legal corridor for recovering underpayment interest and failure-to-deposit levies accrued during the pandemic.

KEY TAKEAWAYS

- Projected Amount: $2,000+ (Variable baseline based on initial IRS penalty assessments).

- Program/Mechanism: Protective Claims under IRC Section 7508A(d) / Kwong v. United States.

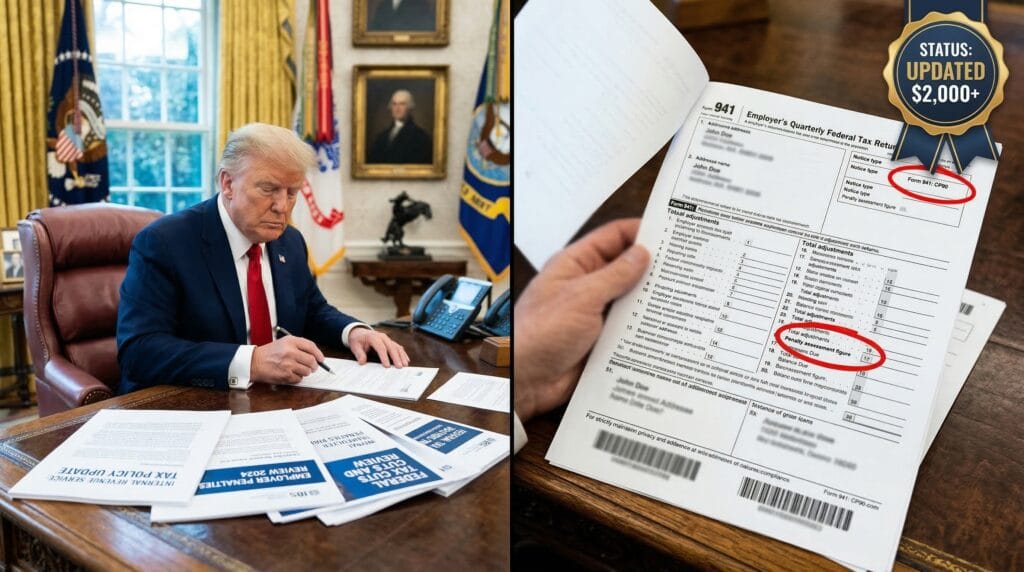

- IRS Notice Type: Form 941 (Requires Form 941-X for amendment).

- Statutory Timeline: Protective claims must be filed by July 10, 2026; direct deposit preference election due by March 31, 2026, for upcoming quarterly processing.

Analyzing the Viral Claims (The Pivot)

Social media platforms are saturated with fragmented information regarding automatic pandemic refunds. Digital algorithms frequently strip away the bureaucratic reality, leaving the public with distorted expectations of immediate capital injection. The prevailing online rumor suggests that the IRS is universally distributing flat $2,000 checks to all California residents who filed taxes between 2020 and 2023.

Legal filings and official Treasury bulletins present a fundamentally different reality. The disbursements are not automatic stimulus checks. They are specific, calculated returns of capital that the IRS previously collected as underpayment interest or failure-to-file penalties during the COVID-19 federally declared disaster period. The recent U.S. Court of Federal Claims ruling in Kwong v. United States determined that the government lacked the statutory authority to accrue these penalties between January 20, 2020, and July 10, 2023. Recovering these funds requires submitting precise protective claims via Form 941-X.

Eligibility & Regional Compliance

| Category | Requirement | Projected Amount |

| Filing Status | Submitted Form 941 between Q1 2020 and Q2 2023. | Variable base |

| Penalty Assessment | Incurred failure-to-pay or underpayment interest. | 100% of assessed interest |

| Jurisdiction | Primary business address in California during the disaster window. | Standard federal rates apply |

| Filing Action | Submission of Form 941-X prior to July 10, 2026. | $2,000+ (Average recovery) |

Institutional Outlook

The intersection of federal tax law and executive policy is reshaping corporate balance sheets across the West Coast. California, having endured one of the nation’s longest continuous disaster declarations, represents the largest concentration of affected entities. The legal framework supporting these capital recoveries rests entirely on the 2019 congressional amendment to Internal Revenue Code Section 7508A(d). This specific statute mandates an automatic extension of tax deadlines following a federally declared disaster.

Because the pandemic was officially classified as a federal emergency, the U.S. Court of Federal Claims ruled that the IRS improperly allowed interest and penalties to accrue against taxpayers during a three-year suspension window. Financial analysts observing the fallout note that the Treasury is now positioned to return billions of dollars in improperly collected capital. The average affected mid-sized California enterprise stands to recover amounts well exceeding $2,000, with some corporate claims reaching into the millions based on their original tax liabilities.

The Trump administration has fundamentally altered how these recovered funds reach the private sector. Executive Order 14247, issued to modernize federal disbursements, mandates that all Form 941 refunds be issued via direct deposit rather than paper checks. This policy shift eliminates the traditional six-to-eight-week postal delay, pushing liquidity back into the commercial sector at a vastly accelerated rate. Tax professionals emphasize that entities seeking to capture these funds must update their banking information with the IRS by the end of the first quarter to ensure seamless routing of their protective claims.

The mechanics of filing for these refunds involve navigating complex bureaucratic channels. The IRS’s handling of payroll tax amendments requires intensive manual review. Since these new Form 941-X filings involve penalty abatement rather than novel credit generation, the adjudication process operates under distinct statutory constraints. Legal experts indicate that the government’s initial defense strategy in these refund suits relied heavily on the statute of limitations. IRC Section 6511 generally restricts refund claims to three years from the filing date or two years from the payment date. The Kwong decision bypassed this limitation by validating the Section 7508A(d) disaster extension, establishing the universal July 10, 2026, boundary.

The economic implications for California’s commercial sector remain substantial. Companies that liquidated assets or took on high-interest debt to satisfy IRS penalty demands during the pandemic now possess a legal mechanism for restorative justice. Institutional observers predict a massive influx of Form 941-X filings as the 2026 deadline approaches, potentially straining IRS processing centers and extending audit timelines for late filers.

PEOPLE ALSO ASK

What is the March 31 deadline for Form 941?

The end of the first quarter serves as the primary cutoff for updating banking credentials under the new federal direct deposit mandate. Missing this window pushes the electronic routing setup into the subsequent processing quarter.

How does the Kwong decision affect commercial taxes?

The ruling established that the IRS could not legally accrue certain penalties and interest during the COVID-19 disaster declaration. Taxpayers who paid these invalid assessments can reclaim the capital through formal amendment filings.

Why is California heavily impacted by these claims?

While the judicial ruling applies federally, California’s prolonged state of emergency and high concentration of commercial enterprises make it the primary geographic center for these specific penalty recoveries.

CHECK OFFICIAL STATUS AT IRS.GOV

Strict Journalistic Disclaimer: This report provides clinical analysis of current legislation, executive orders, and federal court rulings. The information contained herein does not constitute financial, legal, or tax advice. Readers are directed to consult registered fiduciaries or tax professionals regarding their specific institutional or individual filing requirements.

Evan Cole Editor-in-Chief | Breaking News & Public Policy

“From Washington to Wall Street, and Main Street to Hollywood—Evan Cole connects the dots.”

As the Editor-in-Chief at Newskilo, Evan leads a dynamic team of journalists dedicated to uncovering the truth behind the headlines. With over 15 years in digital media, Evan has a reputation for cutting through the noise.

While he is widely recognized for his deep analysis of U.S. fiscal policy (IRS & Stimulus), Evan’s expertise extends to global current events, corporate accountability, and cultural trends. Whether he is breaking down a complex government bill, exposing a tech giant’s failure, or analyzing the societal impact of a viral celebrity moment, Evan’s goal is simple: To tell the stories that shape our world with clarity, accuracy, and integrity.