AUSTIN, TEXAS —

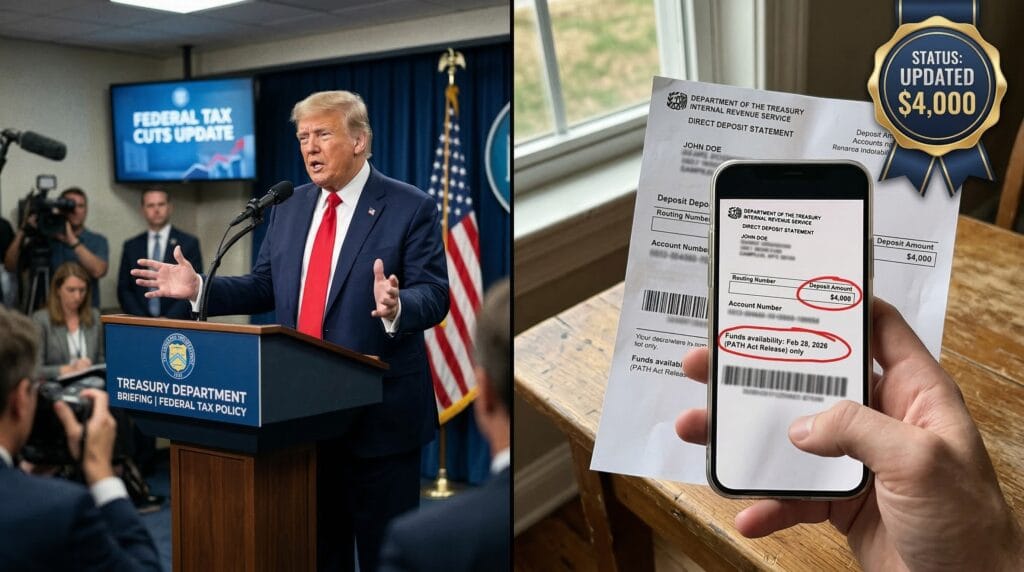

Millions of early tax filers across Texas are witnessing the immediate release of substantial federal capital following a weeks-long institutional embargo. The Internal Revenue Service has formally dismantled the statutory hold mandated by the Protecting Americans from Tax Hikes (PATH) Act. This legal pivot unblocks an average of $4,000 in Earned Income Tax Credit (EITC) and Additional Child Tax Credit (ACTC) refunds for qualifying households, with primary direct deposit waves officially clearing financial institutions on or before March 2, 2026.

KEY TAKEAWAYS

- Projected Amount: $4,000 (Average baseline EITC distribution).

- Program/Mechanism: Earned Income Tax Credit (EITC) / PATH Act statutory release.

- Notice Type: IRS Direct Deposit / Form 1040 Schedule EIC.

- Timeline: Federal embargo lifted mid-February; primary disbursements routed by March 2, 2026.

Analyzing the Viral Claims (The Pivot)

Digital networks frequently distort the mechanics of federal taxation. Social media platforms across Texas recently amplified narratives suggesting the IRS had permanently confiscated EITC returns to offset national debt. The prevailing online rumor positioned the delay as a punitive measure against early filers, generating immediate institutional panic among low-to-moderate-income households relying on the seasonal capital injection.

The statutory reality operating within the federal tax code contradicts this digital panic. The delay is neither novel nor arbitrary. The PATH Act of 2015 legally prohibits the Treasury from issuing refunds containing the EITC or ACTC before mid-February. This pause exists entirely to combat systemic identity theft and fraudulent wage reporting. The Trump administration’s oversight of current IRS protocols ensures these compliance checks conclude precisely when the law dictates. Once the mandated timeline expired following the Presidents’ Day holiday, the federal ledger instantly authorized the transfer of billions of dollars. The $4,000 average disbursements arriving now represent the mechanical execution of the law, rather than a sudden government concession.

Eligibility & Regional Compliance

| Category | Requirement | Projected Amount |

| Filing Status | Submitted Form 1040 claiming EITC prior to mid-February. | Variable base |

| Credit Limit | Federal maximum peaks at $8,231 for families with 3+ dependents. | $4,000 (State Average) |

| Jurisdiction | Texas state residency established within federal tax filings. | Standard federal rates apply |

| Distribution Date | PATH Act freeze lifted; primary routing cleared by March 2. | Immediate Liquidity |

Institutional Outlook

The structural mechanics of the U.S. tax refund apparatus represent one of the largest seasonal wealth transfers in the global economy. For decades, the EITC has functioned as a primary antipoverty mechanism, effectively operating as a negative income tax for working-class populations. The integration of the PATH Act into this system introduced a mandatory friction point, forcing millions of households to navigate a predetermined liquidity drought during the first quarter of the fiscal year.

Texas occupies a unique position within this federal framework. The state lacks a localized income tax infrastructure, meaning its labor force relies exclusively on the federal return for seasonal capital injections. Demographic density and regional income averages dictate that a massive proportion of the Texas service, manufacturing, and agricultural sectors qualify for varying tiers of the EITC. Economic analysts observing this demographic concentration note that the staggered release of these funds profoundly alters regional retail cycles. When the federal freeze lifts, billions of dollars flood the Texas consumer market simultaneously, temporarily shifting macroeconomic consumption metrics.

The $4,000 figure frequently cited in institutional reporting represents a median statistical baseline rather than a universal flat payout. The complexity of the EITC calculation heavily weighs the number of qualifying dependents against earned income thresholds. While individuals without children may see returns measured in the hundreds, households claiming three or more dependents frequently command maximum distributions exceeding $8,200 for the 2026 tax year. The aggregation of these specific credits consistently positions Texas as one of the largest aggregate recipients of federal EITC funding in the nation.

Executive branch oversight heavily influences the physical distribution of these assets. The Trump administration has prioritized modernizing the Treasury’s disbursement architecture. Legacy paper checks, which previously subjected rural Texas populations to extended postal delays, are increasingly marginalized in favor of direct electronic routing. By forcing the majority of EITC refunds through Automated Clearing House (ACH) networks, the federal government compresses the timeline between the expiration of the PATH Act hold and the moment funds become accessible to the consumer. Financial institutions across Dallas, Houston, and San Antonio reported processing immense volumes of these standardized ACH transfers precisely at the March 2 cutoff.

Tax professionals emphasize the rigidity of the IRS processing schedule following the mid-February unlock. The agency processes returns in batch cycles, prioritizing early electronic filers who provided valid routing and account numbers. Submissions complicated by secondary schedules, suspected identity flags, or mathematical errors remain trapped in a manual review queue, bypassing the initial release window entirely. For the vast majority of compliant filers, the bureaucratic machinery operated exactly within its statutory boundaries, transforming frozen tax credits into liquid capital immediately upon legal authorization.

PEOPLE ALSO ASK

Why did the IRS hold my EITC refund until late February?

The PATH Act of 2015 legally mandates that the IRS retain any tax refund claiming the Earned Income Tax Credit or the Additional Child Tax Credit until mid-February to verify income and prevent systemic tax fraud.

Is the $4,000 EITC payment a flat amount for everyone?

The distribution varies significantly based on individual tax circumstances. The federal formula calculates the specific payout using earned income levels, filing status, and the exact number of qualifying dependents.

What happens if my direct deposit did not arrive by March 2?

Returns requiring manual review or those submitted via paper format operate outside the accelerated direct deposit window. The IRS maintains an electronic tracking portal to monitor individual processing statuses for delayed disbursements.

CHECK OFFICIAL STATUS AT IRS.GOV

Disclaimer: This report provides clinical analysis of current legislation, executive orders, and federal tax protocols. The information contained herein does not constitute financial, legal, or tax advice. Readers are directed to consult registered fiduciaries or tax professionals regarding their specific institutional or individual filing requirements.

Evan Cole Editor-in-Chief | Breaking News & Public Policy

“From Washington to Wall Street, and Main Street to Hollywood—Evan Cole connects the dots.”

As the Editor-in-Chief at Newskilo, Evan leads a dynamic team of journalists dedicated to uncovering the truth behind the headlines. With over 15 years in digital media, Evan has a reputation for cutting through the noise.

While he is widely recognized for his deep analysis of U.S. fiscal policy (IRS & Stimulus), Evan’s expertise extends to global current events, corporate accountability, and cultural trends. Whether he is breaking down a complex government bill, exposing a tech giant’s failure, or analyzing the societal impact of a viral celebrity moment, Evan’s goal is simple: To tell the stories that shape our world with clarity, accuracy, and integrity.