ALBANY, NEW YORK — Millions of New York taxpayers are encountering a permanent structural addition to the 2026 federal filing season. A persistent claim sweeping across metropolitan parenting groups alleges that the federal government is issuing immediate $1,000 cash deposits for recent births. The figures dominating these localized discussions represent a massive overhaul of federal child welfare policy implemented by the Trump administration. The actual legislative text reveals a distinctly different financial reality for families navigating the newly introduced federal trust parameters.

KEY TAKEAWAYS

- Viral Claim: Immediate $1,000 direct cash deposit for New York newborns.

- Verified Amount: $1,000 locked initial Treasury contribution.

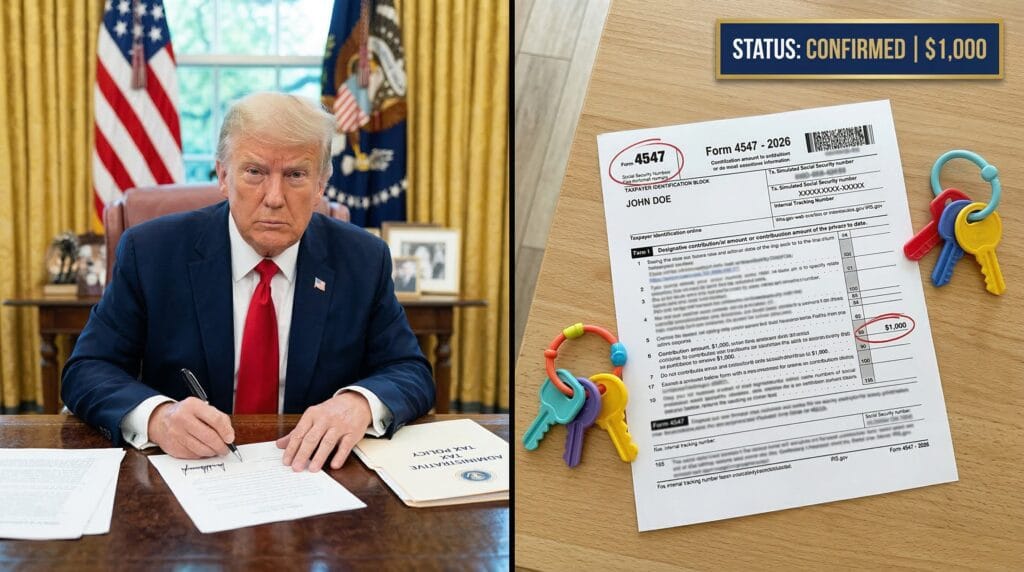

- Notice Type: IRS Form 4547 / Notice CP12.

- Timeline: Claimed actively during the 2026 tax filing season.

Analyzing the Viral Claims

Social media channels across the five boroughs recently amplified reports of a direct $1,000 stimulus check arriving for new parents. Analysts observe that this specific dollar figure relates directly to the newly enacted “Trump Account” pilot program. The current legislative framework operates under a trust-based parameter rather than a direct liquid cash disbursement. The systemic rollout of this program in a high-tax state like New York creates unique financial planning variables. State tax authorities must now differentiate between standard federal refunds and the creation of these restricted federal assets.

The law authorizes a federally managed investment account seeded with an initial $1,000 for eligible children born within the specified administrative window. The conflation of direct pandemic-era stimulus checks with this new restricted-access trust account generated the widespread misunderstanding currently dominating New York digital forums. The $1,000 figure repeatedly surfaces in regional news broadcasts, often stripped of its vital regulatory context.

IRS operational data indicates that parents cannot simply withdraw these funds for immediate expenses. Federal law requires the Department of the Treasury to hold and invest the principal until the child reaches adulthood. Taxpayers filing their 2026 returns are now establishing the legal framework for these accounts rather than claiming an immediate tax refund enhancement.

Eligibility & Regional Compliance

The transition to the new federal trust framework requires strict adherence to updated IRS guidelines. The agency deployed revised documentation to handle the permanent changes to dependent claim structures.

| Category | Requirement | Projected Amount |

| Birth Year Eligibility | Born in calendar years 2025-2028 | $1,000 principal deposit |

| Filing Requirement | IRS Form 4547 attached to return | Establishes federal ledger |

| Income Threshold | MAGI below state-adjusted limits | Full eligibility if under limit |

| Viral Rumor | Immediate direct cash payment | $0 (Funds restricted in trust) |

Institutional Outlook

The permanent authorization of a $1,000 federal seed account signals a significant structural shift in generational wealth policy. Institutional watchers note that this specific transition requires stringent compliance from state-level health departments. The updated federal mandate requires coordinated data sharing between New York vital records offices and the IRS. This closes previous administrative gaps that allowed delayed Social Security Number registrations. This specific adjustment alters the procedural timeline for parents, heavily impacting hospital administration workflows across the state.

The introduction of Form 4547 adds a layer of unprecedented complexity to the 2026 tax filing season. Filers must affirmatively elect to establish these new federal accounts simultaneously with their annual income declarations. The federal government estimates these procedural changes will establish billions in locked capital over the next decade. Early projections from the Congressional Budget Office indicate the pilot program requires highly coordinated sovereign wealth management from the Department of the Treasury. By indexing the base deposit to a federally managed bond portfolio, the administration aims to anchor future domestic purchasing power for the next generation.

The systemic overhaul directly targets the foundational wealth disparities historically observed in urban centers like New York City. By forcing capital into a locked Treasury vehicle, the administration bypasses the immediate consumer economy. Economists evaluating the Manhattan and Albany metropolitan data sets suggest that state-level supplementary programs may eventually mirror this federal architecture. The structural reality of the new policy forces a clinical recalculation of childhood financial planning. This localized economic pressure fundamentally alters the operational strategy of every family law practice functioning within the state.

Financial institutions operating within New York are actively modifying their advisory protocols based on these new federal guidelines. The banking sector reports massive consumer inquiry volume regarding the tax implications of the trust growth. The Treasury Department maintains that all generated interest within the “Trump Accounts” remains tax-exempt until authorized withdrawal. Discrepancies between the claimed birth dates on standard returns and the verified federal vital records trigger automatic holds. This frequently results in the issuance of an IRS Notice CP12. The data confirms the tax code is functioning as legislated, systematically establishing the $1,000 trusts rather than distributing the rumored liquid cash sums.

PEOPLE ALSO ASK

Can New York parents spend the $1,000 deposit right away?

Federal law dictates that the $1,000 deposit is locked in a Treasury-managed trust account. The funds are not accessible for immediate parental spending or everyday child-rearing expenses. The account matures when the designated beneficiary reaches the legal age defined by the pilot program parameters.

What happens if I forget to file IRS Form 4547 this year?

Form 4547 is the mandatory official documentation required to establish the account for eligible newborns. Filing this form retroactively requires a formal tax amendment process. Financial analysts observe that failing to file during the child’s birth year delays the initial investment accrual period.

Does the $1,000 newborn account replace the standard Child Tax Credit?

The newly established trust accounts operate entirely independent of the standard Child Tax Credit. The federal government processes the standard monthly or annual tax credits separately from this one-time $1,000 capital injection. Both programs coexist within the 2026 federal tax code.

CHECK OFFICIAL STATUS AT IRS.GOV

Disclaimer: This report provides a clinical analysis of legislative updates and institutional tax policy. It does not constitute financial, legal, or tax counsel. Consulting official government resources or certified professionals is standard practice for verifying individual filing status and dependent eligibility.

Evan Cole Editor-in-Chief | Breaking News & Public Policy

“From Washington to Wall Street, and Main Street to Hollywood—Evan Cole connects the dots.”

As the Editor-in-Chief at Newskilo, Evan leads a dynamic team of journalists dedicated to uncovering the truth behind the headlines. With over 15 years in digital media, Evan has a reputation for cutting through the noise.

While he is widely recognized for his deep analysis of U.S. fiscal policy (IRS & Stimulus), Evan’s expertise extends to global current events, corporate accountability, and cultural trends. Whether he is breaking down a complex government bill, exposing a tech giant’s failure, or analyzing the societal impact of a viral celebrity moment, Evan’s goal is simple: To tell the stories that shape our world with clarity, accuracy, and integrity.